TSI #2.6: WFE Financials And Valuation Analysis

TSI #2.6: WFE Financials And Valuation Analysis

Summary

This report is the final part of the WFE section of TSI - bringing together all the previous research in TSI #2.X.

Despite short-term disappointments, the semiconductor industry is undergoing various secular shifts, and WFE is a key enabler.

We summarise the market positioning of six WFE vendors, compare financials and financial trends, and conduct valuations.

The TL;DR is KLA Tencor, followed by Applied Materials, looks like the most attractive WFE long-term investments right now.

Latest Quarter Recap

The narrative across the major WFE names is that they are succeeding in making gradual improvements in operations and supply chain management, though, the overall conditions remain very challenging. Generally, the expectation is that supply constraints will persist deep into CY23, though incremental adjustments will continue to have a positive impact.

Each WFE vendor also shares the experience that consumer demand has materially softened. This has affected logic and memory; however, the latter, with it being more cyclical, has been hit harder, leading to memory chipmakers scaling down capacity plans. In the long run, the WFE vendors still have high confidence thanks to the ongoing technology inflections. Those that involve bringing greater performance like EUV and transistor shrinkage, 3D gate architectures, and advanced packaging, as well as those demand drivers like auto, IoT, 5G, and HPC (High Performance Compute). In summary, while there is greater volatility, there will be continued capex in cutting-edge and mature nodes, but in the near-term memory demand will decline.

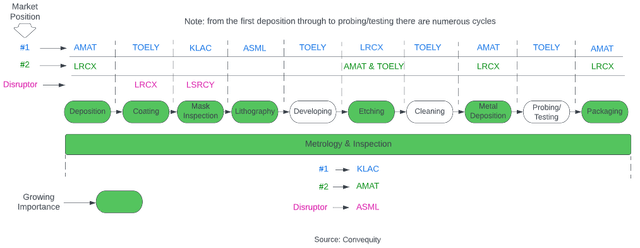

Market Positioning Analysis

We’ll begin the analysis by summarising the market strengths of each WFE vendor, because this will help us assess their respective outlooks and hence help guide the growth factor in the valuations. The diagram below lists the #1 and #2 vendors, as measured by market share/position, to each section of WFE. You’ll notice a few empty spaces in the #2 spots: this is because the #2 is a vendor we haven’t covered and we thought it would be better to only include the names we’ve covered so far.

We’ve also added the Disruptor which has the potential to challenge the incumbent leaders. The sections highlighted green are the ones that seem destined to grow in importance during the next few years – which actually includes the majority.

Source: Convequity

At a glance, AMAT and LRCX are in strong market positions at present; both are either #1 or #2 in a number of WFE sections that are growing in importance. AMAT is the unquestioned leader in the deposition category, and more specifically, PVD (Physical Vapour Deposition) and ALD (Atomic Layer Deposition). PVD and ALD are becoming increasingly important for advanced packaging that requires shorter and denser interconnects and wiring. Backside power distribution is another technological innovation, hoping to deliver big performance improvements, in which AMAT can capitalise on with its deposition leadership. On the whole, we consider AMAT in a strong position with a low risk factor, and as you’ll see later, this is incorporated in the valuation process.