Updates - FTNT - Early Signs Of Macro Headwinds But Long-Term Sound

Updates - FTNT - Early Signs Of Macro Headwinds But Long-Term Sound

FTNT's 2Q22 ER was a shock to investors, but we believe the impact is more short-lived vs. the long term thesis.

Summary

On 1st August, FTNT 0.00%↑ released a good ER but didn't beat expectations and gave some clues that there may be macro resistance ahead.

Despite potential short-term headwinds, the demand for hybrid-capable vendors, converged security/networking, and vendor consolidation, will perpetuate long-term growth.

In this report we highlight FTNT's vision and execution in key fields, including its security-driven networking, Zero Trust, and emerging SecOps market.

No Great News = Bad News

The headline for FTNT does not look great. Fortinet falls 16% as outlook drags down security stocks (NASDAQ:FTNT) Posting a no surprise ER, in a time when investors are in the risk-off mode, triggered a selloff in the shares of more than 16%. We continue to see a wide slash in valuations for software and tech names in general. Although we believe FTNT's results for this quarter show continued strength, apparently it is not good enough to induce a risk-on sentiment in the way NET did.

Our insight here is that investors should keep the big picture in mind while the majority of investors are chasing the fad. The earnings call was of the archetypical form whereby analysts focus mostly on asking questions about non-strategic matters so they can tweak their short-term models. As the adage goes, 'the devil is in the detail', so such lines of inquiry have their place, but for us it definitively shows that,

A. Investors are increasingly cautious and concerned about macro headwinds.

B. Investors are looking for short-term results and are hyper reactive to changes which may or may not be a good indicator of long-term results.

C. Analysts are focusing on fine tuning their models ready for the next quarter instead of thinking about strategic vision and execution.

We sense that this short-term perspective is more prevalent across less-covered stocks and/or companies with less buzz around the long-term vision.

Alpha opportunity from better understanding of the business

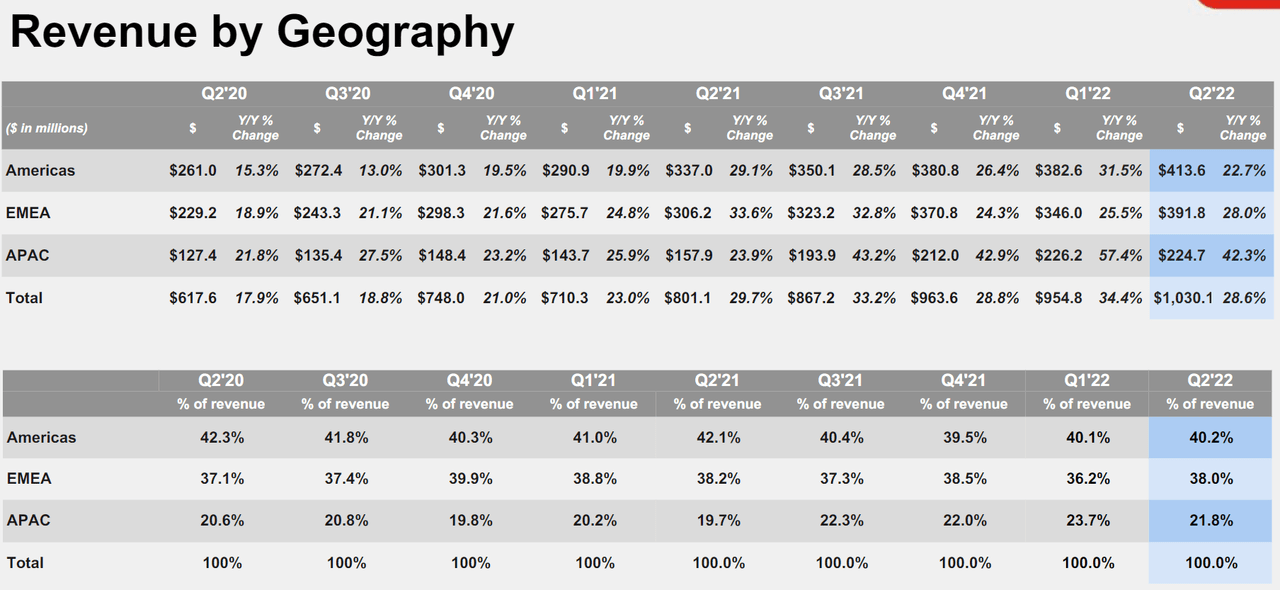

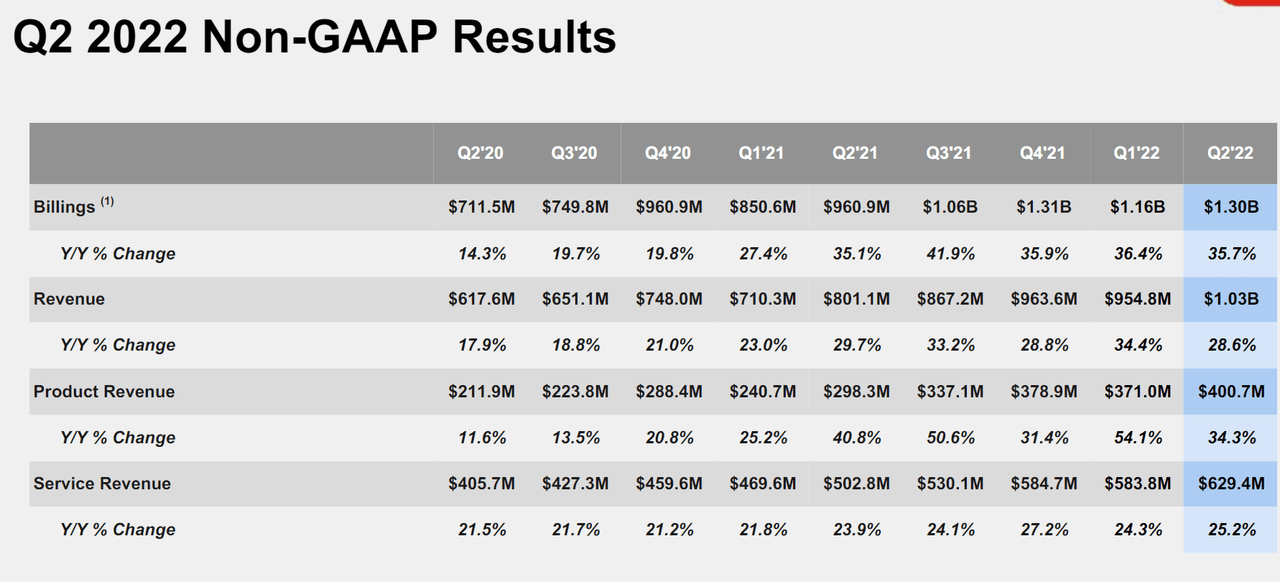

Both revenue and EPS were inline with the consensus. However, management provided soft guidance citing longer sales cycles to land deals, and possible short-term headwinds to service revenue.

Subsequently, analysts became deeply worried about the demand for the next quarter, asking if the refreshment cycle has ended (hence product revenue's 54% growth in last quarter didn't continue), if the weak guidance is an indicator that the business is turning, if seasonality and backlog factors are abnormal as they fish for data points to update their model (another indicator of weak sentiment and less caring of product fundamentals).

Thus, we believe an update on FTNT's fundamentals is useful for investors to gain an edge over street analysts who are overly focused on very short-term results.

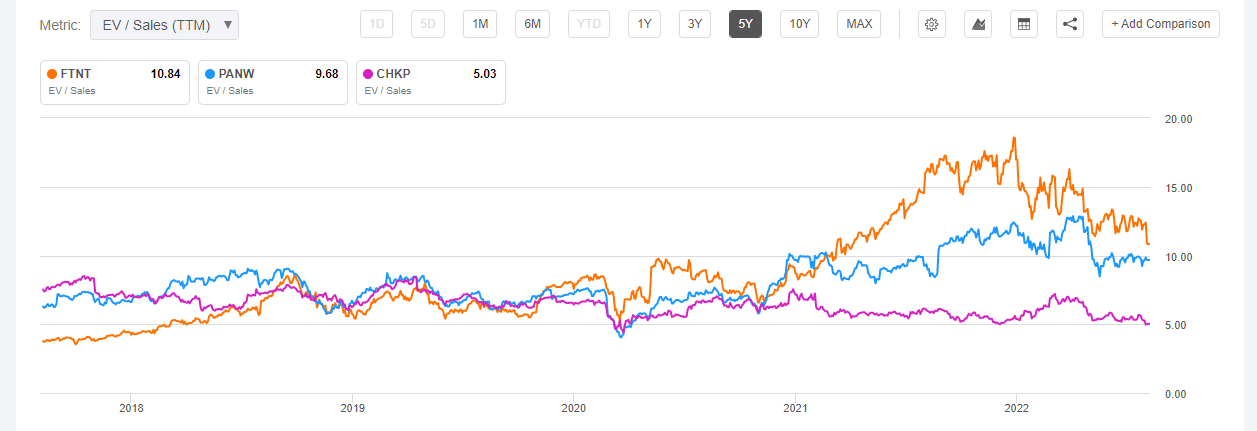

Fortinet, Inc. (FTNT) Charting

Vision and Execution

A key to FTNT's strong investor returns for the past couple of years has been its durability of growth with strong profitability. There isn't that many companies who can keep c. 30% growth for several years after it was founded more than a decade ago while keeping the operating margin at 20%+, creating huge numbers of new products with modest R&D spending, and returning high amounts of cash via buybacks.

We continue to like FTNT's "always day-one" vision of where the market is heading and invest in R&D resources to develop home-grown BoB solutions. Furthermore, this is empowered by a unique set of talent with ASIC and hardware know-how (rare in the software-centric world), a strong footprint in Canada and China and the rest of the world (to lower costs), and an engineering culture that focuses on building new solutions quickly and efficiently. All of these result in better shareholder returns.

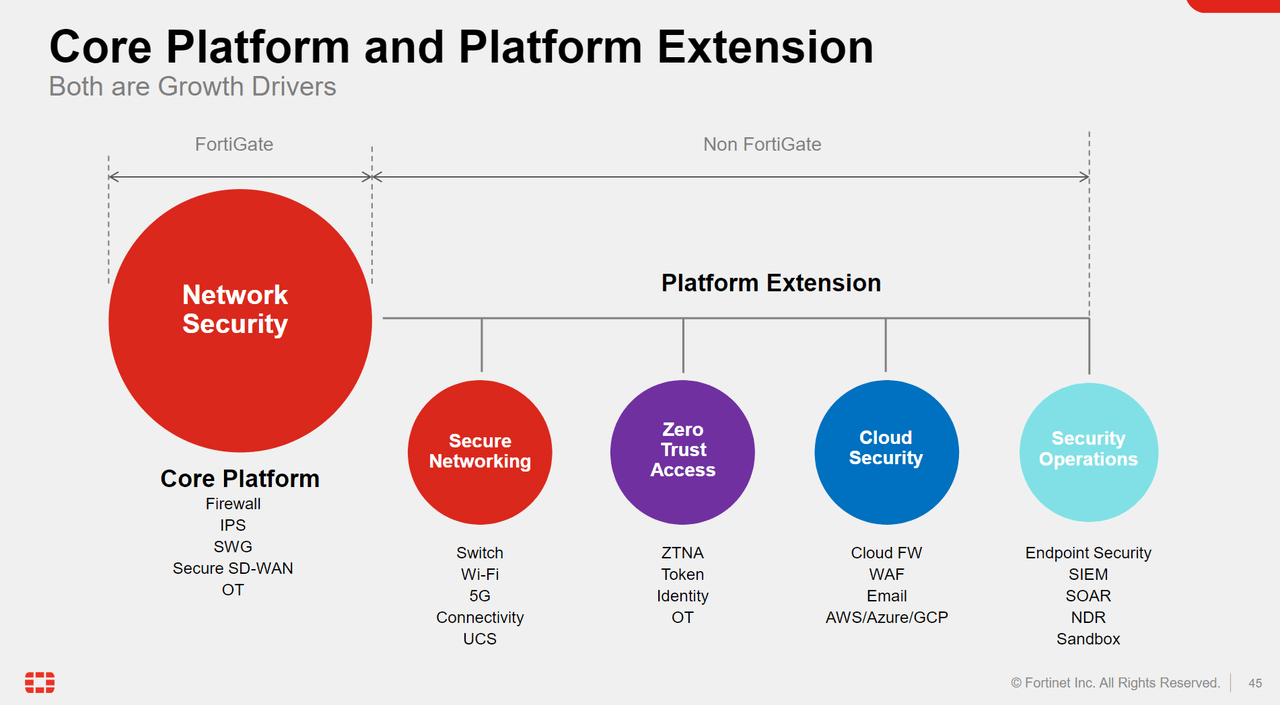

FTNT breaks down its product offerings into one network security platform, and four adjacencies including networking, ZTA, cloud security, and SecOps. We will briefly discuss each in the next sections.

Security and Networking

One particular visionary move that we saw from FTNT is its venture into SD-WAN. Back in 2019, FTNT was mostly a SMB-focused NGFW vendor. Unlike many other cohorts like Sophos, however, FTNT continues to innovate and target bigger markets. In this case, they saw the forthcoming SD-WAN opportunity was brewing. FTNT correctly foresaw the strategic importance of SD-WAN as the final piece of CPE (Client Premise Equipment) required, and a value-add to its existing NGFW business. We believe this continues to be a multi-year theme to unfold and evolve.

Why? If SD-WAN is going to be the future, it could be the only WAN Edge CPE required for many enterprises. You don't need a dedicated NGFW, load balancer, application steering device etc., - numerous boxes chained together in the server room. Instead, these individual networking functions can be virtualized (Network Function Virtualization, or NFV) and run as independent software within the single SD-WAN box. This is not only for inside out but also for Telcos, who service tremendous amounts of users. It could eliminate the need for multiple hardware installations, time-consuming maintenance, and reserve precious space in cellular towers. Should SD-WAN continue its strong momentum, NGFW vendors could get smoothed out in the future. FTNT is the only vendor able to envision this great opportunity early on, while PANW only played catch up in 2020 by acquiring CloudGenix, a second-tier software-focused SD-WAN vendor during the liquidity crisis.

Furthermore, the foundational technology behind SD-WAN is the IPSec tunnel that allows enterprises to get rid of pricey MPLS and instead procure commercial broadband connectivity for their WAN. Coincidentally, IPSec acceleration is a key part of FTNT's ASIC, and therefore, with simple code changes, FortiGate NGFW can turn into powerful SD-WAN CPE offering IPSec throughput at orders of magnitude more scale than a similarly priced x86-based COTS (Commodity Off-The-Shelf) CPE.

When FTNT entered space, there wasn't too m