Full Report - QCOM - Connectivity is the Future (1/2)

Unlike NVDA, QCOM’s potential seems to be underappreciated.

Welcome to Covequity's Quick Takes— Timely interpretation of news & special events for cybersecurity and enterprise tech investors. If you are new, you can join our email list here:

Sources of Alpha: Complexity of the Business

Expected Price Appreciation: 100% from $180 within 3 years

Executive Summary

Huawei competition threats and antitrust lawsuits are now behind QCOM.

A recently appointed CEO with a technical background replaces the former CEO that was overly focused on cutting costs that made QCOM trail in chip performance.

Connectivity tailwinds linked to autos, IoT, VR, and others will provide solid growth for QCOM.

The recent Nuvia acquisition combined with the secular tailwinds is finally putting QCOM back on the right path.

We view QCOM as having the potential to deliver a minimum 2x return during the next 2-3 years.

Contents

Article 1 (Free Preview Available)

A Brief History of QCOM

QCOM Before the Antitrust Lawsuits

Competition and the Future

Article 2 (Paid Subscriber Only)

Valuation Considerations

Some Key Terminology

RFFE – stands for Radio Frequency Front End, but commonly referred to as the RF-front end. The RF-front end is located in a mobile phone in order to receive radio frequency signals and then transmit the signals to the modem.

Modem – interprets the data received from the RF-front end and translates it to the phone’s CPU [Central Processing Unit] for computation.

SOC – stands for System-On-Chip and incorporates the CPU [Central Processing Unit], the GPU [Graphics Processing Unit], and other chip components.

SEP – stands for Standard Essential Patent. This is a patent that must be used by industry stakeholders in order to adhere to a technical standard.

QTL – stands for Qualcomm Technology Licensing. QCOM has numerous patents pertaining to radio frequency protocols that it licenses out to smartphone manufacturers and other equipment vendors.

QCT – stands for Qualcomm CDMA Technologies and incorporates the design of the RF-front end, modems, and the SOCs. QCOM sells these as part of its semiconductor operations.

Summary

In the past, thanks to a rich pack of patents, QCOM has completely dominated the mobile telecommunications market since the early 1990s. However, in a similar vein to INTC, due to weak competition QCOM barely innovated since 2010. Then, when 4G & LTE came along it was the beginning of QCOM losing its grip as it suffered anti-trust lawsuits and alternatives emerged for smartphone manufacturers.

A bleak outlook rolled into the beginning of the 5G era as Huawei had a superior radio frequency code that outperformed QCOM. Moreover in 2021, QCOM’s latest Snapdragon 888 chip has a relatively poor performance that underscores the lack of innovation in recent years. Luckily for QCOM, Trump’s ban on Huawei, despite its shortcomings, helped it become the number one choice again for high-end Android device manufacturers desperate to catch up Apple – we’re not just talking mobile phones, but wearables and smart speakers and various other consumer IoT.

QCOM has secured its cash cow of high-end Android smartphones by being the number one choice. Though, the greenfield opportunity is in the Intelligent Connected Edge – consisting of automotive, PC & servers, virtual reality, and various IoT use cases – in which QCOM has profound competitive advantages due to its superior capabilities in connectivity. Undoubtedly, the major secular tailwind to drive all these tech advancements is 5G and whether or not the high frequency technology can live up to its promises. In simple terms, if 5G can deliver in a timely manner, then the thesis for QCOM is super bullish.

To summarize, the thesis for QCOM is all about connectivity >>> vehicle connectivity, IoT connectivity, VR connectivity, because it simply has the best modem technology and a history of billions of dollars invested radio frequency wave R&D. In particular, we like QCOM’s positioning for the automotive market – whilst NVDA is all about AI powering AD [autonomous driving], it looks like QCOM is targeting the underappreciated side of connected vehicles which is the infotainment aspect. QCOM’s connectivity skillset has the ability to greatly enrich the in-car user experience without competing directly with NVDA.

QCOM’s multiples are in line with low growth semiconductor companies, yet has grown revenues 55% for FY21 [fiscal year ending 30th September] and future growth expectation is in the high-teens. The antitrust stigma, questionable decisions by the former CEO, and being in the shadows of NVDA and AMD has greatly suppressed QCOM’s multiples. But it’s a moderate growth company, with high margins, and a particular growth runway that is less crowded than other mobile telecommunication and chip companies.

A Brief History of QCOM

QCOM creates telecommunication signal protocols and designs mobile phone RF-front ends, modems, and SOCs, and licenses out the patents to smartphone manufacturers. It initially rose to success in the early 1990s when founder Irwin Jacobs envisioned the then-underused radio network access technology, CDMA [Code Division Multiple Access], was going to be the optimal access technology to power 2G and 3G telecommunications.

1G, 2G, and 3G Dominance

1G telecommunications technology was built upon FDMA [Frequency Division Multiple Access] and was mostly used in analog systems. FDMA splits the frequency band into multiple channels to allow one base station to serve multiple users on the same frequency. One user occupies one channel for the duration of the call, and then the channel is handed to the next user. However, dividing the frequency band affects the quality of delivery and reduces the bandwidth.

In the 1990s, 2G technology predominantly utilized TDMA [Time Division Multiple Access], which kept the frequency channel intact but divided it by time – meaning users would need to take turns in sending data [i.e., the first user sends some data and then allows other users to send data before it is their turn again]. TDMA allows each user to access the entire radio frequency channel thus quality of delivery and bandwidth is preserved and the base station is constantly switching the channel between users to manage the scarce resource effectively.

In the 1990s, Jacobs recognized the potential in CDMA - which until then had been predominantly used by the military - to power the 3G evolution. CDMA users access the whole bandwidth for the entire duration [no time slots] and their signals are isolated from one another by code.

Figure 1 - Multiplexing Techniques Across 1G, 2G, and 3G Telecommunication

Source: itu.int

As most competitors we’re not going down the CDMA route, QCOM cultivated somewhat of a monopoly in the U.S during the 1990s. Hence when CDMA adoption began accelerating, QCOM made substantial royalties from telecommunication equipment manufacturers, mobile phone makers, and carriers.

As 3G emerged as the standard in the 2000s, QCOM also began to monopolize the EU as the region adopted Wideband CDMA. Then, QCOM received another tailwind – the introduction of the iPhone in 2007 – which generated more demand, higher selling prices, more use cases, and consequently more use of 3G and CDMA. This confluence of drivers reached a climactic peak for QCOM just prior to GFC, when it grew revenue 26% to $11.1bn.

4G and the End of Dominance

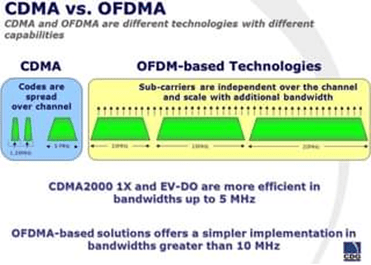

When 4G technology emerged, many telecommunication equipment vendors, smartphone manufacturers, and carriers, were very eager to get away from QCOM’s patent-rich stronghold and switch from CDMA to OFDM - which is the signal format for 4G LTE [Long-Term Evolution].

Figure 2 - CDMA vs OFDMA

Source: m.facebook.com

Not only did QCOM’s excessive milking trigger customers to switch to OFDMA, it caught the attention of regulators. Billions of fines were settled with China, Japan, Korea, EU, US and other countries, and QCOM was forced to give better terms to licensees.

QCOM Before Antitrust

QTL Division

Before the antitrust intervention, QCOM charged 5% of mobile phone shipping prices for all device manufacturers and c. 3% of the shipping price for the license fee. As QCOM holds the majority of SEPs [standard essential patents] in CDMA and other technologies that are fundamental to 2G and 3G, equipment manufacturers and carriers had no alternative but to pay the price.

The complexity in license agreements doesn’t end there, however. As QCOM has monopolized 2G and 3G, it was able to coerce licensees to reverse license their patents to QCOM’s license pool. What that means is if Vendor A pays QCOM for the license, as part of the deal, all of Vendor A’s patents will be part of QCOM’s license to other vendors. Therefore, if Vendor B pays QCOM for the license as well, then it no longer needs to worry about patent infringement with Vendor A. These reverse patent agreements made QCOM something like a Godfather character in the telecommunication space.

QCT Division

QCOM also made the modem chips for mobile phones. The modem enables the device to receive and transmit signals with the surrounding base stations. It decodes the signal received from the RF front-end and forwards it to the AP [application processor] for further processing. The quality and functionality of a modem determines which network the device can connect to, e.g., 3G or 4G, Vodafone or Orange or AT&T or Verizon.

Due to its excessive control in the CDMA space, QCOM had almost exclusive rights to make these modem chips for the CDMA network. Other vendors had to either buy QCOM’s license to design their own CDMA-compatible modem, or they had to buy QCOM’s modem which also had license agreements attached. It really is no wonder that regulators eventually investigated QCOM.

Moreover, what added further to QCOM’s competitive advantages was its c. $30bn in R&D accumulated over three decades, which culminated in them producing the best modem with high interoperability and with the highest number of frequency bands, whilst delivering the best signal strength and lowest power consumption.

As a result, even the most powerful vendor like AAPL has to pay hefty royalties and fees to QCOM for patent licensing and the modem chip. Other vendors do not share the same luxury as AAPL, who is able to afford a modem chip [c. $45] that is as expensive as the AP [c. $50] or SOC [SOC here basically refers to AP + modem]. As such, QCOM's Snapdragon chip - the SOC that integrates modem, CPU, GPU, DSP, ISP, NPU and others all together - becomes the most popular and only choice for non-entry-level [5G enabled] Android phones since the early 2010s.

Competition and Future

5G Standard and Huawei

When it comes to 5G, the environment of vendor lock-in has almost evaporated. Customers loathed QCOM for a long-time but without a realistic alternative until generations later when QCOM’s SEPs started to expire and non-QCOM technology began to emerge.

After CDMA, coding becomes the most viable route, the coding algorithm has become the new battle field. Shannon capacity is the significant determinant here. It provides the theoretical foundation for the maximum data transmitting capacity within a noisy channel. Better forward error correction code means data transmission can reach closer to the limit of Shannon capacity amid the noisy channels that we all encounter during the daily life with multiple radio interfering with each other.

Huawei's Polar code emerged as the dark horse in the 5G eMMB [enhance mobile broadband] standard, as it secures the standard for the control channel [used to transmit protocol and signal information between wireless network nodes], while the LDPC [low-density parity-check] code, backed by QCOM and others, becomes the data channel [used to transmit user information like speech and data] standard by only a very close margin – in fact, had Lenovo and its subsidiary Motorola voted for Huawei, QCOM could have lost by a landslide.

Huawei's bet on Polar code is very much like QCOM's historic bet on CDMA. And Huawei controls 2/3 of the Polar code patent whilst QCOM doesn't have the dominant control over LDPC [low-density parity check] like it did in the past with CDMA.

In terms of the phones and other consumer devices, Huawei is also making a great success. Its HiSilicon custom chip division has rapidly evolved and mimics AAPL's custom chip strategy but with a better modem as the company has the telecommunication equipment background.

Huawei successfully launched its 5G modem earlier than QCOM, and its SOC that integrates state-of-the-art modem offers better performance relative to the highest end Snapdragon. This is due to Huawei's relentless effort in innovation and custom chip status that allows it to design more expensive chips without worrying as much about costs like QCOM does.

QCOM has been too focused on operating expense control and on its 2019 investor day, the CFO even laid out the plan to improve the operating margin from 19% to 30%. As such, QCOM’s chip design team has had its budget slashed and R&D spend has tilted toward the modem side of business. Furthermore, to keep gross margin elevated, it has to make chips at a lower cost, lower area size, and this has resulted in lower performance.

Thankfully for QCOM, Huawei's rapid upsurge ended abruptly when the Trump administration issued the ban predicated on national security concerns. Resultingly, for now, we believe there is no one who can compete with QCOM in regards to the SOC for the modem and Android device. There is also no other vendor who can compete QCOM on patent licensing. Additionally, after the anti-trust settlement, QCOM's QTL business is well secured on regulatory side as well.

AAPL - an Indirect Catalyst to Strengthen QCOM's Ecosystem

In the world of phone chips, now that Huawei is banned from the U.S., QCOM doesn't have a direct competitor. However, the Android phone represents 85% of the market that has c. $300 in ASP [Average Selling Price]. AAPL on the other hand, has 15% market share but c. $900 in ASP thanks to its premium strategy. With 3x the selling price, AAPL is able to design its own chip with the most advanced processes for higher performance and lower power. Premium Android phones have no choice but to go with QCOM, waiting for the launch of every year's latest generation of Snapdragon’s high-end 8 series chip so manufacturers can remain competitive against AAPL.

Similar to INTC back in the 2010s, due to lack of competition, year over year QCOM's chip has barely improved in performance. More outrageously to tech enthusiasts, QCOM's 2021 flagship chip, Snapdragon 888, delivers an actual performance decline compared to the previous year’s 865 chip. And this was due to shifting to the lower cost and lower quality Samsung process from TSMC as well as zero change in the GPU architecture. In real life tests, 888 even trails AAPL's A12 chip that was launched in 2018 - three years ago! And by a wide margin.

Though, the weakness in mobile chip doesn't stop QCOM from being the only choice for premium Android phones. And QCOM’s position is further enhanced by the eagerness to catch up AAPL leading to Android players fighting over each other to become the first to launch the latest Snapdragon chip each year.

The reality is that QCOM has become the only choice for mobile makers competing with AAPL; it is also the only choice for IoT device makers who compete with AAPL. Apple Watch led the wearable tide of demand; Home Pod led the trend for smart speakers at home; Air Pod led the trend for wireless earbuds. If manufacturers want to compete with AAPL but don’t have the ability to design their own chip, QCOM is their only choice to:

buy a smart watch chip with integrated modem,

to buy an earbud chip with the best Bluetooth connection,

and to buy chips for various other IoT devices that need cellular, Bluetooth and WiFi connectivity.

In essence, QCOM has become the ecosystem partner for AAPL's competitors by providing chips, standard design, and software framework. In this way, QCOM secured its competitive edge and we don't think it’s going to fade away anytime soon as the wireless world is the future, and AAPL doesn't sell its chips to others.

Intelligent Connected Edge

In a similar vein to the proliferation of mobile phones, with 5G's MTC [Machine Type Communication – broad use cases that involve things like sensors for smart buildings/homes whereby lighting, heating, etc., are controlled] add-on, more devices will be connected. Wearables and IoTs are just the beginning that takes 1/4 of QCOM's revenue now. QCOM is very likely to be successful in repeating its success in the mobile chip space as connectivity is at the heart of most cases and QCOM has the monopoly over the modem.

QCOM predicted that this new market called Intelligent Connected Edge will collectively increase its SAM by 7x (serviceable instead of total addressable market, as some market space is occupied by vendors like AAPL who designs chips exclusively for themselves). We believe this is largely true and could even be underestimated as the wireless and connected device markets will possibly grow at an accelerating speed once other devices rise up like iPhone did post 2007.

Automotive

At the centre of the Intelligent Connected Edge market is automotive and connected vehicles. NVDA is the biggest player in the automotive chip space, whilst TSLA, much like AAPL, puts its magic sauce on custom chips. Our quick conclusion is that, NVDA's competitive advantages are overpriced and QCOM's potential is underestimated. NVDA's market cap has gone up from $200bn to $800bn in a matter of years thanks to its applications in AI and more specifically, in supplying AI inference chips to automotive vendors.

Aside from autonomous driving, we believe Electric Vehicles could improve the user experience dramatically by adding5G connection to the car, thus enabling the software-defined vehicle paradigm. Furthermore, existing ICE [Internal Combustion Engine] cars' infotainmentsystems are terrible and trailing behind mobile phones by more than 5 years.

Connectivity and know-how in consumer electronics is QCOM's core competence. And there isn’t a second competitor in the foreseeable future except TSLA and AAPL's potential car. Here let’s do a quick thought experiment - in 5 years, what do you think you would value more, autonomous driving or better infotainment, connectivity and overall digital experience with your car? We believe the latter may be underestimated. And if this is the case, then QCOM could take a huge chunk of the pie - but not all, as NVDA will co-exist with QCOM with the former dominating AI and the latter dominating the user experience with its connectivity superiority.

Furthermore, we view there as being a vastly greater imagination space with respect to connectivity and automotive. There are rolls of cable inside connected cars that could weigh 100kg+ and are prone to errors [because of heat, water, dust, bugs, etc.]. QCOM could create ethernet for these parts and connect them wirelessly. This is just the tip of the iceberg and we believe the connectivity will only become more important in the future.

This competitive edge is very subtle. Most of us don't realize how preferable wireless solutions are before we use it. Another simple thought experiment - if you have wireless charging for all your electronics, and wireless connection for all your electronics, would you ever go back to wires all over the place? The answer is clearly no and we believe this is probably the biggest value backstop for QCOM in the years to come.

PC and Servers

This is one of the most exciting part as AAPL has been innovating a new S-Curve again. With M1 chip in 2020 and M1 Pro and M1 Pro Max released recently, AAPL is finally taking the Arm chip into the PC space. This has been a long overdue move as Arm chip's huge volume has induced faster iterations, and hence, better performance improvements. That combined with its superior power efficiency, has opened up the opportunities, especially in power efficient-sensitive applications like laptops and servers.

QCOM has been trying to break into the server market with its Centriq SOC, launched to the market in 2017. What is unfortunate for long term investors, however, is that the interim CEO chose profitability over long-term development and fired the entire team just after the first generation of server chip was launched.

In respect to laptop chips, QCOM has been partnering with various vendors, most notably, MSFT's own Surface laptops. Though, the result has been lacklustre or close to a total failure, due to the complete lack of close collaboration between QCOM and MSFT. QCOM didn't even bother to design a new chip for the MSFT’s Arm-based Surface laptop. Instead, it just repackaged its older 2-3 generations mobile Snapdragon chip into a new chip series for Arm-based laptops.

To put it in context, mobile chips usually have a 10W maximum power consumption whilst laptop ones can endure 30W+ power consumption. By using an old mobile chip instead of a new one specifically designed for the laptop, QCOM's chip is very weak in performance compared to INTC's. This is even worse compared to AAPL's M1, considering QCOM's mobile chip is already 2-3 years behind AAPL. The M1 chip is specifically designed for 30W power consumption, with the architecture also leading QCOM's latest chip by 2-3 years, and the area size 2x-3x of QCOM's as AAPL makes the chip by itself.

The end result is AAPL's arm laptop chip has at least 10x+ power efficiency compared to QCOM's laptop chip - 2.5x due to better design, 2x due to QCOM using a 2-year-old chip, 2x due to AAPL using the latest TSMC process with a huge area size.

Despite all these flaws and mishaps in QCOM’s approach to some aspects of its business over the years, things are changing this year with a new CEO with a technical background. QCOM acquired Nuvia, the company founded by former head of Apple Silicon and its senior engineers. Nuvia's roadmap is super aggressive - bring in a step function-like improvement to all CPUs. Considering AAPL's track record, we believe Nuvia has very high potential to deliver a result at least on par to AAPL's chip and the possibility of producing the best CPU is also very high.

If Nuvia can deliver its promise, then this is a new world for QCOM - it may well take over a large chunk of PC and server market in the future and that would be an incremental $200bn market cap at least.

QCOM is expecting the Nuvia-designed CPU & SOC to be shipped in 2022 and it’s poised to be used in autos and mobile phones in 2023, possibly using INTC's latest 18A process. If these plans can be well executed, QCOM's leadership across all spaces could be heightened to a new level.

Further into the future, mobility is also the mega trend in the PC space. This is evident by the shipment and popularization of laptop vs. desktop, not only for light-weight ones but also pro gaming high-performance ones. If 5G can deliver its promise, there is no need to even install a router within your home because broadband is everywhere, and under such a scenario cellular connectivity could be more important than WiFi. Again, this would be super bullish for QCOM.

Virtual Reality

VR and metaverse related devices are a close adjacency to mobile phones as well. Like AI, VR has gone through multiple rounds of hype and the recent peak was in c. 2013 when Oculus came out with an evolutionary VR experience. The structure of these devices is pretty simple and actually quite close to a phone. A VR lens, for example, is basically a smartphone with a screen attached to two lens’ fitting the viewing space of one pair of eyes. As such, Google Cardboard and Samsung Gear are designed as a pair of lens’ plus a holding structure allowing for a phone to be plugged in.

Figure 3 - Google Cardboard

Source: medium.com

It doesn't cost QCOM anything to rename its older generation Snapdragon mobile chip to a specialized chip for VR as well. QCOM called it XR, and the latest XR2, is basically the same chip as Snapdragon 865 [QCOM's flagship mobile chip in 2020] with a different name. XR2 is used by Oculus Quest 2, the most successful VR set to date, reaching 1 million headsets shipped last year.

Unlike AI, the VR hype has cooled down since 2013 and there isn't much interest to make custom chips for VR. Therefore, we believe this is another market where QCOM could dominate again. The only risk, is that FB may now mimic AAPL's trick in developing a custom designed chip, and furthermore, AAPL could make its own VR sets in the future as well.

The incoming 5G and hyper-connectivity could also help VR as you will no longer be confined within your WiFi connected home, but will be able to go outside with a cellular network. Furthermore, you may be able to get your lens connected with your friends, or your more powerful PC at home, or a processor in the cloud for better gaming experience.